Who Is Selling America?

The 10-Year Treasury Yield and What It Means for Capital Allocators

Why the 10-Year Yield Rules the World

Two days ago, the yield on the 10-year US Treasury note touched 4.65%. It has since pulled back to 4.56% - a move that generated relief across trading floors from New York to Tokyo. That a two-day, nine basis point swing in a government bond yield can move global markets tells you everything you need to know about why this number matters.

The 10-year US Treasury yield is the closest thing global finance has to a universal constant. It is the world's benchmark risk-free rate, the return an investor can earn by lending money to the United States government for a decade, with essentially zero default risk. Every other asset in the world is priced relative to it. Corporate bonds trade as a spread above it. Mortgage rates track it almost in lockstep. Equity valuations are discounted against it. Private equity hurdle rates, LBO financing costs, and emerging market capital flows all move in its shadow.

When the 10-year yield rises, the cost of capital rises everywhere simultaneously - for governments, for corporations, for homebuyers, and for PE sponsors trying to finance an acquisition. When it falls, the reverse is true. It is, in the most literal sense, the metabolic rate of the global economy.

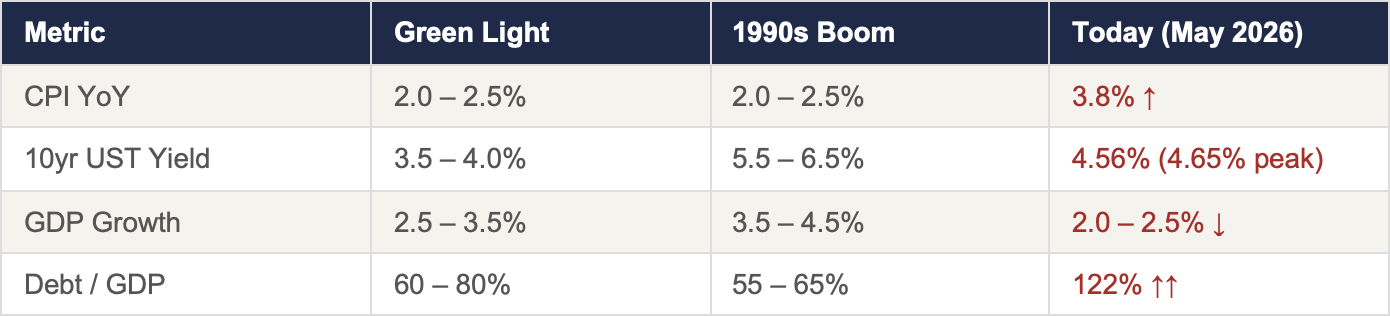

For most of the past decade, capital allocators could treat this number as background noise. The post-2008 era of near-zero rates made cheap money the default assumption baked into every model, every valuation, every fund return. That era is over. The 10-year yield has not been below 4% since late 2023, and as we will argue in this note, the structural forces keeping it elevated are neither temporary nor easily resolved.

Understanding why the yield is where it is, and where it is going, is no longer optional for anyone allocating capital in 2026.

How We Got Here — Five Years of Rising Yields

The 10-year yield does not move in straight lines, but since 2021 the direction has been unmistakably upward. Understanding why requires separating two distinct stories that are often conflated: the inflation shock that started the move, and the fiscal deterioration that has sustained it.

The inflation story is familiar. COVID-era stimulus was unprecedented in both scale and mechanism. Unlike the quantitative easing of 2008, which largely stayed trapped in bank balance sheets inflating asset prices rather than consumer ones, the 2020 stimulus went directly into household accounts. More money chasing fewer goods, against a backdrop of broken supply chains, produced exactly what Economics 101 predicts. Inflation peaked at 9.1% in June 2022. The Federal Reserve responded with the most aggressive rate-hiking cycle in forty years, eleven consecutive increases, and the 10-year yield moved from near zero to above 4% in under two years.

Most observers assumed that once inflation was tamed, yields would fall back. They haven't. The reason is the second, more structural story: the US fiscal position is deteriorating in ways that are increasingly difficult to ignore.

The United States is running an annual deficit of approximately 7% of GDP - in peacetime, in a growing economy. Total national debt stands at $39 trillion, equivalent to roughly 122% of GDP. That ratio was 57% in 2000. It was 98% as recently as 2024. The trajectory is not a gradual drift - it is an acceleration. Interest payments alone now exceed $1 trillion annually, surpassing defence spending. The Congressional Budget Office projects that number rising to $2.1 trillion by 2036, consuming an ever-larger share of every tax dollar collected. The US is, in the most straightforward terms, borrowing money to pay interest on money it has already borrowed.

To finance that deficit, the Treasury must continuously flood the market with new bonds. More supply with a shrinking natural buyer base means lower prices and higher yields - basic bond mathematics with no elegant solution.

In May 2025, Moody's stripped the United States of its last AAA credit rating - a status held since 1919 - downgrading it to Aa1, bringing it in line with S&P and Fitch who had downgraded in 2011 and 2023 respectively. For the first time since World War I, the world's largest economy holds no triple-A rating from any major agency. Moody's was explicit: successive administrations and Congress have failed to agree on measures to reverse the trend of large annual fiscal deficits and growing interest costs.

The symbolic importance should not be understated. For decades, US Treasuries were bought almost automatically as the world's unquestioned safe asset - buyers demanded little premium because American creditworthiness was beyond question. That automatic buyer base is thinning. And increasingly, investors are pricing in risks they previously ignored - not the risk that America defaults, but the risk that its fiscal trajectory becomes genuinely difficult to manage.

For context: only three entities in the world currently hold a Moody's Aaa rating — Microsoft, Apple, and Johnson & Johnson. Their bonds trade at barely 50 basis points above equivalent Treasuries. The gap between sovereign and corporate risk, once vast, is narrowing.

The 10-year was already sitting uncomfortably above 4.5% before the events of early 2026. What happened next turned an uncomfortable situation into an urgent one.

The Macro Dashboard - Where We Stand

The 4.5% Line - Bessent's Tripwire

Not all yield levels are equal. When the 10-year Treasury crosses 4.5%, something specific happens in Washington: alarm bells ring and the Treasury moves into active intervention mode. Understanding why requires a brief look at the mathematics of American debt.

The US government must refinance trillions of dollars of existing debt every year as bonds mature - in addition to issuing new bonds to cover the ongoing deficit. At 4.5%, that refinancing cost is manageable, painful but sustainable. Every 50 basis points above that level adds roughly $200 billion in additional annual interest costs across the debt stock as it rolls over.

At 5%, the interest bill becomes structurally unmanageable without either printing money, cutting essential spending dramatically, or some combination of both. The debt spiral, where higher yields force more borrowing which forces yields higher still, becomes self-reinforcing above that threshold. This is the specific nightmare Bessent is trying to prevent.

Treasury Secretary Scott Bessent has been explicit: his focus is on the 10-year yield, not the Fed's overnight rate. This is a deliberate and historically unusual choice. Most administrations defer to the Federal Reserve on interest rate matters. Bessent has essentially declared that managing the long end of the curve is a Treasury function - and that 4.5% is the line he will defend. Wall Street has taken note, shifting from the old adage of "don't fight the Fed" to "don't fight the Treasury."

When the line breaks, Bessent acts. The specific tools he deploys, and the longer-range plays he has quietly set in motion, are covered later. What matters here is the stakes: every basis point above 4.5% costs the US government approximately $4 billion annually per trillion dollars of debt outstanding. With $39 trillion on the books, the arithmetic is unforgiving.

The 3-3-3 plan - Bessent's broader ambition to cut the deficit to 3% of GDP, grow the economy at 3%, and add 3 million barrels of daily oil production - is a fascinating and ambitious economic strategy that deserves its own dedicated analysis. For the purposes of this note, what matters is the immediate tactical picture: a Treasury secretary defending a line, with real but limited tools, against forces that are partly structural and partly geopolitical.

Who Is Selling America - and Why It Matters

Two days ago the 10-year Treasury yield touched 4.65%. The move was not random. Behind every yield spike is a seller - and understanding who is selling, and why, reveals something far more consequential than a routine bond market fluctuation.

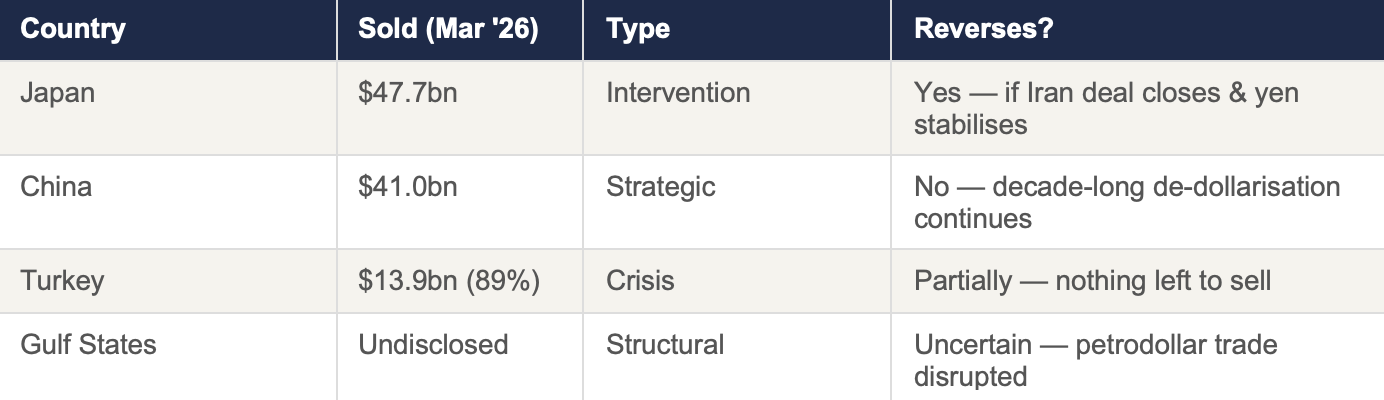

The US Treasury Department publishes monthly data on foreign holdings of US government debt - the Treasury International Capital report, known as TIC data. The March 2026 figures, released just days ago, tell a striking story. Total foreign-owned Treasuries fell from a record $9.487 trillion in February to $9.348 trillion in March - a $139 billion decline in a single month. Seven of the top ten foreign holders reduced their positions simultaneously. This does not happen by accident.

Japan - $47.7 billion sold

The world's largest foreign holder cut its position by nearly 4% in a single month. The reason is mechanical but consequential: the Iran war sent oil prices above $100 a barrel, dramatically widening Japan's energy import bill and weakening the yen toward the politically sensitive 160 level. To defend its currency, the Bank of Japan sold Treasuries, converted the dollars to yen, and bought yen in the open market. This is currency intervention - temporary in theory, but Japan has been forced to repeat it repeatedly as energy costs remain elevated.

China - $41 billion sold, holdings at lowest since 2008

China's position tells a more complex and more important story. The $41 billion sold in March brought its total holdings to $652 billion - the lowest level since September 2008, and down 14% since the start of 2025 alone. The official explanation is short-term market volatility driven by the Iran conflict. That explanation is technically accurate and almost certainly incomplete.

China has been on a deliberate, decade-long de-dollarisation strategy since its peak Treasury holdings of $1.317 trillion in 2013. The reduction has been gradual and carefully paced - fast enough to reduce dependency, slow enough not to trigger the self-destructive consequences of a sudden dump. The Iran war provided legitimate cover to accelerate that pace. But the timing deserves scrutiny.

The March selling occurred in the weeks immediately preceding the Beijing summit of May 14-15. China walked into that summit having already quietly reduced its Treasury exposure to a 17-year low.

Our reading: the selling served as implicit negotiating leverage - a demonstration that China holds levers it can pull without triggering mutual destruction. It didn't need to threaten anything explicitly. The TIC data spoke for itself to anyone paying attention.

This is the financial weapon that rarely gets discussed openly. China doesn't need to dump its entire position to inflict pain - the weapon is more surgical: gradual, deniable, always attributable to market conditions, but directionally consistent with geopolitical pressure points.

Turkey - 89% of its entire position liquidated

The most dramatic single-country move in the data. Turkey went from $15.7 billion to $1.8 billion in one month - a near-complete liquidation. This was pure crisis management: the Iran war sent shockwaves through Turkey's economy, the lira came under severe pressure, and Ankara sold everything it could to defend its currency. Unlike China's strategic patience, Turkey's selling was panic. It is also largely irreversible in the near term as Turkey has nothing left to sell.

Saudi Arabia and the UAE

Both Gulf states reduced their positions as the Iran war disrupted the petrodollar recycling mechanism - the decades-old arrangement where oil revenues are converted to dollars and parked in US Treasuries. With the region in active conflict and oil revenues being redirected toward defence and domestic stabilisation, the automatic Treasury buying that underpinned this arrangement stalled. This is a structural shift with implications beyond the immediate crisis.

Who Is Selling

The Three Seller Types

The selling breaks into three distinct categories with very different implications for what comes next.

Crisis sellers: Turkey, India, Thailand, were responding to acute economic pressure. Their selling reverses when the crisis passes.

Intervention sellers: Japan, are defending currency levels and will rebuild positions if energy prices fall. These two categories are largely Iran-dependent and could reverse on a deal.

The third category - strategic de-dollarisers, led by China - does not reverse. This is the slow-burn story beneath the dramatic headlines. Every month, quietly and with plausible deniability, the world's second largest economy reduces its exposure to American sovereign debt. The natural buyer base for US Treasuries is structurally thinner than it was a decade ago and getting thinner still.

The 30-year Treasury briefly touched 5.12% this week - its highest level since 2007. The market is not just pricing stress for the next decade. It is pricing it for the next generation.

What the Treasury Does When the Line Breaks

The yield touching 4.65% earlier this week was not met with silence in Washington. It rarely is. The move back toward 4.56% over the past two days is not purely organic - it reflects a Treasury that, true to form, reached for its toolkit the moment the tripwire was crossed.

The most immediate lever is debt composition. The Treasury has significant discretion over how it finances the deficit - specifically, the ratio of short-term Treasury bills to long-dated bonds it issues each week. By quietly tilting issuance toward bills and away from 10-year and 30-year notes, Bessent reduces the supply of long-dated paper hitting the market. Less supply of 10-year bonds means higher prices and lower yields - basic bond market mechanics, executed without a single press release. This is the "Bessent Put" - the market's shorthand for the Treasury's ability to manage yield levels through issuance composition rather than outright intervention.

The second lever is direct buybacks. The Treasury can purchase its own older bonds in the open market, absorbing supply and supporting prices. This is not QE as it does not involve money creation. The Federal Reserve prints money to buy bonds in QE. The Treasury simply redirects existing funds to repurchase outstanding debt, reducing the float and nudging yields lower. Targeted buybacks of $2–10 billion have been deployed several times in the past eighteen months specifically when the 10-year approached uncomfortable levels.

The third lever is bank regulation. Bessent has been pushing to loosen the Supplementary Leverage Ratio - a post-2008 rule that limits how much long-dated government debt banks can hold relative to their capital base. Loosening it frees up commercial bank balance sheets to absorb more Treasuries, structurally boosting demand from the domestic banking system. This is the slowest lever as it requires regulatory process, but potentially its effect might be the most durable.

Beyond these three immediate tools, Bessent has two longer-range plays in motion. The first is the stablecoin strategy - the recently passed GENIUS Act requires stablecoin issuers to back every digital dollar with US Treasury bills, creating a structurally captive new buyer base that grows automatically as the stablecoin market expands toward its projected $2 trillion by 2028.

The second is the Mar-a-Lago Accord - a deliberate, coordinated weakening of the dollar that makes US exports more competitive, narrows the trade deficit, and reduces the real burden of dollar-denominated debt. The dollar has already fallen roughly 10% in 2025, suggesting the groundwork is quietly being laid.

None of these tools are a substitute for the Federal Reserve's ultimate nuclear option - large-scale quantitative easing, where the Fed creates money to buy bonds in whatever quantity is needed to cap yields. That remains available in a genuine crisis. But deploying it would signal a level of fiscal stress that itself risks accelerating the loss of confidence it is meant to arrest. It is the option that works precisely because it doesn't need to be used.

Bessent is managing a yield problem with surgical tools when the underlying causes - a $39 trillion debt pile, a 7% deficit, sticky inflation, and a thinning foreign buyer base - require structural solutions that are beyond any Treasury secretary's unilateral reach.

The Iran deal, if it closes, is the single most powerful near-term catalyst for structural improvement. Cheaper oil, lower inflation, Fed rate cuts, and a calmer geopolitical environment would do more for the 10-year yield than any of Bessent's technical interventions. Which is why the most important bond market variable right now is not in Washington - it is in the negotiating rooms where the Iran deal is being hammered out.

What It Means for Private Equity and Capital Allocation

For private equity, the 10-year Treasury yield is not an abstract macroeconomic variable. It is the single number that determines the cost of every leveraged buyout, the discount rate applied to every portfolio company valuation, and the return threshold against which every fund is measured. When it moves, the entire PE business model moves with it.

The era that built modern private equity, roughly 2010 to 2021, was defined by one structural gift: falling rates. Cheap debt made LBOs affordable. Falling discount rates inflated exit multiples. Returns were driven less by operational excellence than by the simple mathematics of buying an asset at one multiple and selling it at a higher one as rates fell and valuations expanded. That era is over. It ended in 2022 and it is not coming back in any near-term scenario we can construct.

The consequences are visible in the data. New broadly syndicated LBO loans are currently yielding around 8% - down from 11% in 2023 but still high enough to dramatically change the economics of leverage. A deal that generated a 25% IRR in 2019 with 6% debt financing requires genuine operational value creation to achieve even 15% at today's rates. The financial engineering playbook has been retired not by choice but by arithmetic.

The exit backlog is the most acute symptom of this transition. Only 16.6% of 2021-vintage PE deals have exited by year four - compared to 32.3% of 2017-vintage deals at the same stage. Funds that bought at peak 2021 valuations, underwritten on near-zero rate assumptions, are sitting on assets they cannot sell at acceptable prices without crystallising losses. The Iran war and the yield spike have made this worse - every week of elevated rates extends the period of valuation compression and LP frustration.

The LP pressure is becoming acute. Distributed to Paid-In capital has collapsed across the industry. LPs need distributions to rebalance portfolios, meet liquidity obligations, and recommit to new vintages. This is creating a growing population of motivated sellers: GPs under pressure to exit at any reasonable price, continuation vehicles being rushed to market, and secondary transactions at meaningful discounts to NAV. For patient buyers with dry powder and a long enough horizon, this is the most interesting entry environment in a decade.

Where the Opportunities Actually Are

The firms that navigate this environment best will share three characteristics.

First, genuine operational capability - the ability to grow revenue, improve margins, and create value independently of multiple expansion or cheap debt.

Second, sector focus in areas structurally insulated from or actively benefiting from the current macro environment - energy infrastructure, defence technology, AI-enabled businesses, and private credit.

Third, the discipline to buy distressed or motivated sellers rather than competing in crowded auction processes at full valuations.

Private credit deserves specific mention. As banks retreated from leveraged lending after 2022, private credit funds stepped into the gap. That market now exceeds $2.5 trillion globally and is structurally advantaged in a high-rate environment - floating rate loans mean returns rise automatically as rates stay elevated. For PE firms that have built private credit capabilities alongside their equity strategies, the current environment is generating some of the best risk-adjusted returns in the asset class's history.

The Emerging Markets Contra-Indicator

For NEEM specifically, the current environment contains a counterintuitive opportunity that deserves emphasis. High US yields have driven capital away from emerging markets - investors have chosen the safety of 4.5% risk-free returns over the complexity and currency risk of EM investments. EM valuations have compressed, currencies have weakened, and foreign capital flows have reversed. This feels like a reason to avoid EM. Historically it is the opposite.

The best EM vintage years consistently follow periods of dollar strength and capital outflows - precisely because compressed valuations, weakened currencies, and motivated local sellers create entry points that simply do not exist when global capital is flowing freely into EM assets. When the Iran deal closes, oil falls, the Fed cuts, and the dollar softens, capital will rotate back into emerging markets rapidly. The investors already positioned will capture the re-rating. Those waiting for the all-clear signal will pay full price for assets they could have bought at a discount today.

India is the clearest expression of this thesis. Despite the capital outflows of 2025-2026, India's structural story - demographics, digitisation, manufacturing diversification from China - remains intact and arguably stronger. The rupee weakness that has accompanied the dollar surge creates an additional return kicker for dollar-denominated investors when the cycle turns. Southeast Asia - Vietnam, Indonesia, the Philippines - offers a similar dynamic with the added tailwind of the China+1 supply chain realignment that the Iran war, paradoxically, has accelerated as companies seek supply chain resilience.

The question for capital allocators is not whether to have EM exposure. It is whether to build it now, at distressed valuations, or later, at recovered ones.

What Comes Next - The Three Scenarios

Predicting the precise trajectory of the 10-year yield is a fool's errand. What is possible, and more useful for capital allocation, is mapping the realistic range of outcomes and understanding what each means for PE dealmaking, financing costs, and exit timing over the next 24 months.

The single most important variable in every scenario is the same: inflation. Not the Fed, not Bessent, not foreign selling. If inflation returns sustainably toward 2–2.5%, the dominoes fall in the right direction automatically. If it doesn't, no amount of policy creativity resolves the underlying tension between a $39 trillion debt pile and a bond market demanding adequate compensation to hold it.

Scenario 1 - The Constructive Case (probability: 30%)

10-year yield: 3.5–4.0% by end 2027. The Iran deal closes within weeks. Oil falls back toward $75–80 per barrel. Energy inflation reverses sharply, pulling CPI toward 2.5% by Q4 2026. Warsh gains the political cover to cut rates 75–100 basis points. The 10-year yield drifts toward 3.75% as the term premium compresses and foreign selling stabilises.

For PE this is the scenario that restores deal economics closest to pre-2022 conditions. LBO financing costs fall toward 6–6.5%, exit multiples recover, the exit backlog clears, and LP distributions resume. EM assets re-rate sharply as dollar-denominated capital rotates back. Vintage 2025–2026 looks, in retrospect, like 2009–2010 — the best entry point of the cycle.

Scenario 2 - The Muddle-Through (probability: 50%)

10-year yield: 4.0–4.5% for 2–3 years. The Iran deal produces a partial ceasefire but not a full resolution. Oil falls moderately to $85–90 but doesn't collapse. Inflation stays sticky at 3–3.5%. FED cuts once or twice but stays cautious. The 10-year oscillates between 4.0% and 4.5%, occasionally testing Bessent's tripwire and retreating each time as Treasury intervenes.

For PE it means a persistent adjustment rather than a clean recovery. Deal activity recovers modestly but never regains 2021 peak volumes. LBO economics require genuine operational value creation. The exit backlog clears slowly and selectively. EM recovery is gradual rather than sharp - still positive for patient capital but without the explosive re-rating of Scenario 1.

Scenario 3 - The Stress Scenario (probability: 20%)

10-year yield: 5%+ becomes the new floor. The Iran deal collapses. A second wave of oil price inflation embeds into wages and services. CPI re-accelerates toward 5%. FED is forced to choose between hiking rates - triggering a recession and worsening the debt spiral - or tolerating inflation, destroying its remaining credibility. The 30-year Treasury - already at 5.12% - breaks toward 5.5–6%.

For PE this is a genuine reckoning. LBO financing at 10%+ makes most leveraged transactions mathematically unviable. Portfolio company valuations fall sharply. The exit backlog becomes a crisis rather than a problem. A wave of distressed asset sales creates opportunities for the most well-capitalised players - but the environment for deploying that capital is deeply uncomfortable.

NEEM's Verdict

Our base case is Scenario 2 with asymmetric upside toward Scenario 1 if the Iran deal closes in the coming weeks - which current signals suggest is more likely than not. The 10-year yield settles into a 4.0–4.5% range over the next 12–18 months, gradually drifting lower as inflation cools and Warsh makes measured cuts.

For capital allocators, this is not a moment for paralysis. The uncertainty that feels uncomfortable in the present is precisely what creates the valuation dislocations that generate superior returns in retrospect. The firms waiting for the all-clear - for inflation to hit 2%, for yields to fall to 3.5%, for the exit backlog to clear - will find that by the time those conditions exist, asset prices will have already recovered to reflect them.

The playbook for the next 24 months is clear: operational value creation over financial engineering, private credit as a core allocation rather than a satellite, emerging markets built patiently at compressed valuations, and dry powder preserved for the distressed sellers that a prolonged higher-rate environment inevitably produces.

The 10-year Treasury yield is not the enemy of private equity. It is the market's most honest signal about the state of the world. Right now that signal is telling us that the era of effortless returns driven by cheap capital is behind us - and that the era of returns driven by genuine skill, insight, and operational excellence has begun.

Disclaimer: This Market Note is produced by NEEM Group for informational purposes only and does not constitute investment advice or a solicitation to buy or sell any security. The views expressed reflect NEEM’s analysis at the time of writing and are subject to change. Readers should conduct their own due diligence before making any investment decisions.