T-Zero for Capital Markets

What SpaceX’s Historic IPO Means for the Future of Space Investment

In a matter of hours, for the first time in history, you will be able to buy a share of the company building humanity’s path to Mars.

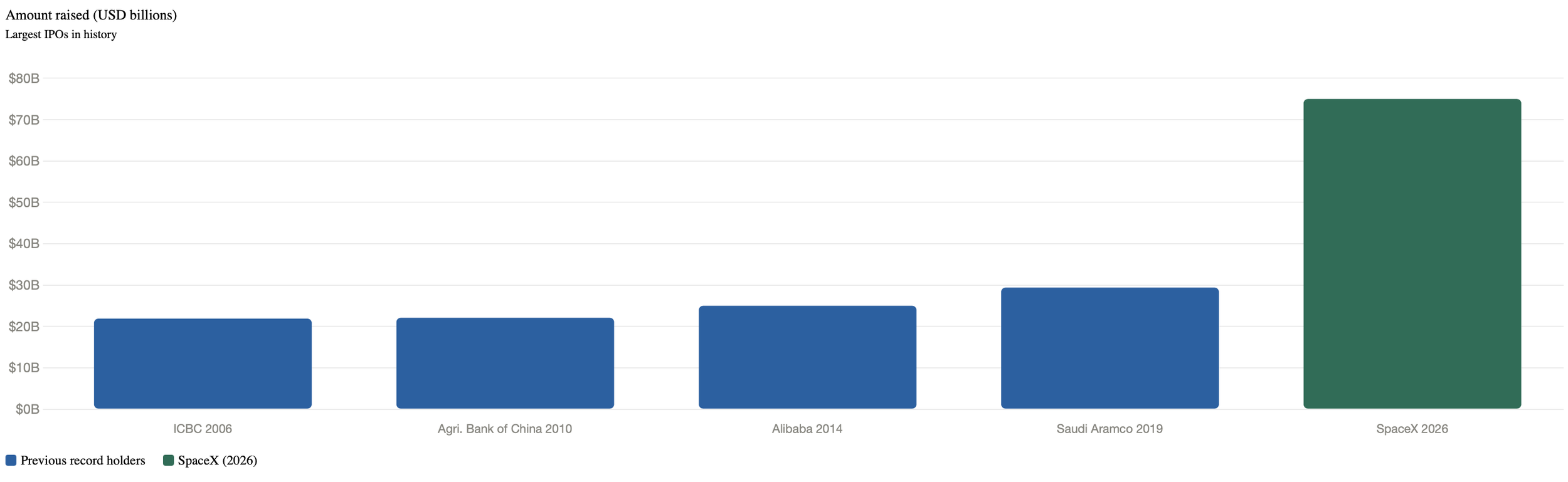

Space Exploration Technologies Corp — SpaceX — is set to begin trading on the Nasdaq under the ticker SPCX on the morning of June 12, 2026. Priced last night at $135 per share, it will complete the largest initial public offering in the history of global capital markets, raising $75 billion at a valuation of $1.77 trillion. With underwriters holding a 30-day option to purchase an additional 83.3 million shares, total proceeds could reach $86 billion.

To put that in context: Saudi Aramco’s 2019 listing, previously the largest IPO ever recorded, raised $29.4 billion. SpaceX raised more than twice that figure before the greenshoe. It is not a marginal record — it is a generational one.

Bar chart comparing the largest IPOs in history by amount raised in billions of USD

The demand confirmed what markets had been signalling for weeks. When the underwriting syndicate — Goldman Sachs, Morgan Stanley, JPMorgan and Citigroup — closed the institutional order books on June 10th, total orders had peaked at approximately $250 billion, roughly 3.5 to 4 times the size of the offering. Multiple sovereign wealth funds, pension giants and mutual fund managers placed individual orders of $10 billion or more. Veteran Wall Street analysts struggled to find a comparable precedent. There isn’t one.

The offering was internally codenamed Project Apex. It is an apt name. What happens on Nasdaq this morning is, by almost any measure, the apex of what a private company going public can look like.

Not a Rocket Company. A Platform.

To understand why a quarter of a trillion dollars flooded into a single order book, you need to understand what SpaceX actually is. The name evokes rockets and astronauts, but the investment case rests on something far broader.

SpaceX today is three distinct businesses operating under one roof, each compelling in its own right, collectively unlike anything public markets have ever been asked to price.

The first is the launch business most people know. SpaceX conducts more orbital launches annually than any other entity on earth, including national space agencies. Its reusable rocket architecture — pioneered when the industry said it was impossible — has driven launch costs down by an order of magnitude and made it the default infrastructure provider for commercial satellite operators, scientific missions and defence contractors alike. NASA is a cornerstone customer. In May 2026 alone, SpaceX won two US Space Force contracts totalling $6.45 billion in the span of four days, cementing its role as the primary contractor for America’s Golden Dome missile defence architecture. These are not one-off wins, they are the beginning of a multi-decade government relationship in a domain that will only grow in strategic importance.

The second business is Starlink — and this is where the investment story becomes genuinely extraordinary. Starlink is a constellation of over 7,500 satellites in low Earth orbit delivering high-speed internet to anywhere on the planet. It generated $11.4 billion in revenue in 2025, at a 63% adjusted EBITDA margin. Subscriber numbers doubled in a single year, from 4.5 million to 10.3 million. It is already being deployed on commercial flights, and the trajectory is clear — within five years, in-flight Starlink connectivity will be the industry standard rather than the premium exception. That is a recurring, high-margin, globally scalable revenue stream that most listed technology companies would envy.

The third business is the one that has Wall Street producing numbers that feel almost fictional. Following SpaceX’s acquisition of Elon Musk’s AI company xAI in February 2026, the combined entity is now positioning itself as the infrastructure backbone of the next generation of artificial intelligence — not on Earth, but above it. Space-based data centres, powered by solar energy in low Earth orbit and free from the power grid constraints throttling AI expansion on the ground, are targeted for deployment as early as 2028. The commercial validation has already arrived: Anthropic has signed a contract paying SpaceX $1.25 billion per month for space-based compute through 2029, and Google followed with a $920 million per month agreement for its Gemini AI platform. Goldman Sachs projects SpaceX’s AI segment alone could generate $322 billion in annual revenue by 2030. Morgan Stanley’s 2040 projection for the entire company: $3.4 trillion in revenue.

This is why traditional valuation frameworks struggle. SpaceX is loss-making at the net level — the xAI buildout consumed $12.7 billion in 2025 and is accelerating — and trades at approximately 104 times trailing sales. But the market is not pricing 2026. It is pricing the platform that 2030 and 2035 will be built on. In that context, the frenzy around this IPO is not irrational. It may simply be early.

There is one further detail worth noting, more for its symbolism than its financial weight. X, the social media platform formerly known as Twitter and acquired by Musk in a chaotic and headline-dominating $44 billion takeover in 2022, has now been absorbed into xAI and — by extension — into SpaceX. It returns to public markets not as a standalone media company but as a footnote inside a $1.77 trillion aerospace and AI conglomerate. The arc is remarkable.

Looking further ahead, speculation is already circulating in investment circles about whether Tesla could eventually merge with SpaceX, forming a single Musk conglomerate spanning electric vehicles, energy, rockets, satellites and artificial intelligence. Nothing is imminent, and Musk has not confirmed any such plans. But for investors thinking in decade-long horizons, the question of how “Musk Industries” ultimately gets packaged — and valued — is not an idle one.

Where Does $250 Billion Come From?

The oversubscription numbers are extraordinary enough to warrant a moment of pause. $250 billion in orders for a $75 billion offering. That capital did not materialise from thin air — it was reallocated, repositioned and in many cases liquidated from somewhere else. The question every institutional allocator should be asking this morning is not just “did I get my allocation?” but “what did the market have to give up to get here?”

The evidence was visible in real time. In the week leading up to pricing, broad equity markets sold off meaningfully. Analysts were explicit about the cause — portfolio managers were trimming existing positions to free up capital for SpaceX allocations. This is the liquidity vacuum in action: a single offering so large that it visibly distorts the market around it in the days before it even trades.

Historical precedent offers some guidance, though none that maps perfectly. The closest comparison is Saudi Aramco’s December 2019 listing — at $29.4 billion, previously the largest IPO on record. The Aramco offering created significant liquidity pressure in Saudi domestic markets, severe enough that the Saudi central bank had to stand ready to intervene, managing a squeeze driven by heavy loan demand from investors seeking to fund their allocations. And Aramco was a largely domestic listing, with a float of just 1.5% on the Saudi exchange, drawing primarily from regional capital pools.

SpaceX is a different animal entirely. It lists on the Nasdaq with a 4% float, drawing from global institutional capital. The absolute scale of reallocation is larger, the investor base broader, and the ripple effects more widely distributed. Where Aramco created a domestic tremor, SpaceX has the potential to register across every major portfolio in the world.

But the more sobering context is what comes next. SpaceX is not an isolated event — it is the opening act of what may be the most concentrated period of mega-listings in capital market history. Both OpenAI and Anthropic have filed paperwork with the SEC for their own IPOs, widely expected later in 2026. Between them, these three companies represent the defining businesses of the AI era, and markets will be asked to absorb all three within a twelve month window. One senior investment executive, quoted this week, put it plainly: “Record new issues is one of the classic signs of a bubble.”

That may prove too pessimistic. But the liquidity arithmetic is real regardless of whether one is bullish or bearish. $250 billion chasing SpaceX alone. Two more historic listings in the pipeline. And a float so thin — just 4% of shares in circulation today — that genuine price discovery for SPCX will take months, not hours. The first real test comes in September, when employees become eligible to sell 20% of their holdings following the first earnings report. That is the moment the market finds out what SpaceX is actually worth when supply meets unconstrained demand.

For now, what trades today is something closer to a signal than a price. And the signal is unambiguous: institutional capital wants in, at almost any cost.

The Unclogging Effect

For the private equity and growth equity community, today’s listing represents something more structurally significant than a headline valuation. It represents the arrival of an exit.

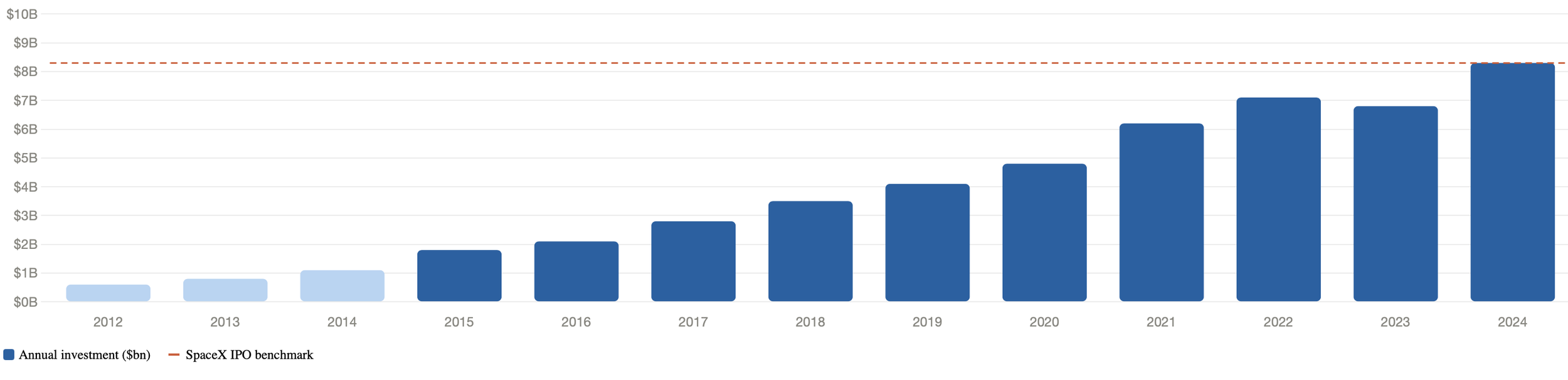

Space, until this morning, was a sector without a credible public market benchmark. Venture capital and growth equity funds had been deploying into space companies for a decade — global investment grew from under $2 billion annually before 2015 to $8.3 billion in 2024 — but always against a backdrop of uncertainty about how and when that capital would come back.

Bar chart showing annual PE and VC investment in space companies from 2012 to 2024

There were no liquid public comparables of meaningful scale. No IPO pipeline. No established strategic acquirer with a public currency to use in acquisitions. Exits were possible in theory but difficult to model in practice, which kept institutional PE capital cautious and kept the sector disproportionately reliant on venture funding.

That changes today.

Starlink’s 63% EBITDA margin and SpaceX’s implied revenue multiples now give every satellite connectivity business, orbital infrastructure company and space data platform a pricing anchor. A growth equity investor modelling an exit for a portfolio company in 2030 can, for the first time, point to a liquid public comparable and build a credible case. That is not a small thing. In private markets, the availability of a public comp is often the difference between capital flowing freely into a sector and capital sitting on the sidelines waiting for permission.

This is what we mean by the unclogging effect. The dam has not broken — but the blockage that was holding back a significant volume of institutional PE deployment has been removed. Expect the pace of growth equity investment into mid-stage space companies to accelerate meaningfully over the next 24 months as fund managers update their return models with reference to today’s pricing.

The structure of that investment will look different from traditional PE. Space is not a buyout sector — the companies are too capital intensive, too early in their maturity curves, and too dependent on continued R&D investment to suit a leveraged acquisition model. What fits is growth equity: Series B through pre-IPO rounds, typically with 5 to 7 year horizons, often structured with strategic corporate limited partners alongside institutional capital. Seraphim Space, the most prominent dedicated space fund, counts satellite operators Arabsat and Eutelsat alongside NEC and UK government institutions among its LPs — a model that blends financial and strategic capital in ways that suit the sector’s particular dynamics. AE Industrial Partners has taken a similar approach on the US side, backing Redwire Corporation and York Space Systems as growth equity plays within a broader aerospace mandate.

The sweet spot for PE deployment is specific. It sits in the middle of the capital stack — companies that have proven their technology, secured initial government contracts, and demonstrated operational credibility, but remain too capital intensive for venture cheque sizes and too early in their earnings trajectory for traditional buyout. These businesses need patient, sizable capital and operational partnership. They are, in other words, precisely what growth equity is designed for.

SpaceX’s IPO does not just validate the sector. It provides the exit architecture that makes the whole investment case cohere. The question is no longer whether space is a real asset class. It is whether your portfolio has exposure to it.

The Industry Behind the Rocket

SpaceX is the pioneer. But the industry it has catalysed is far larger than any single company, and it is the infrastructure beneath the headline that represents the most compelling long-term investment opportunity.

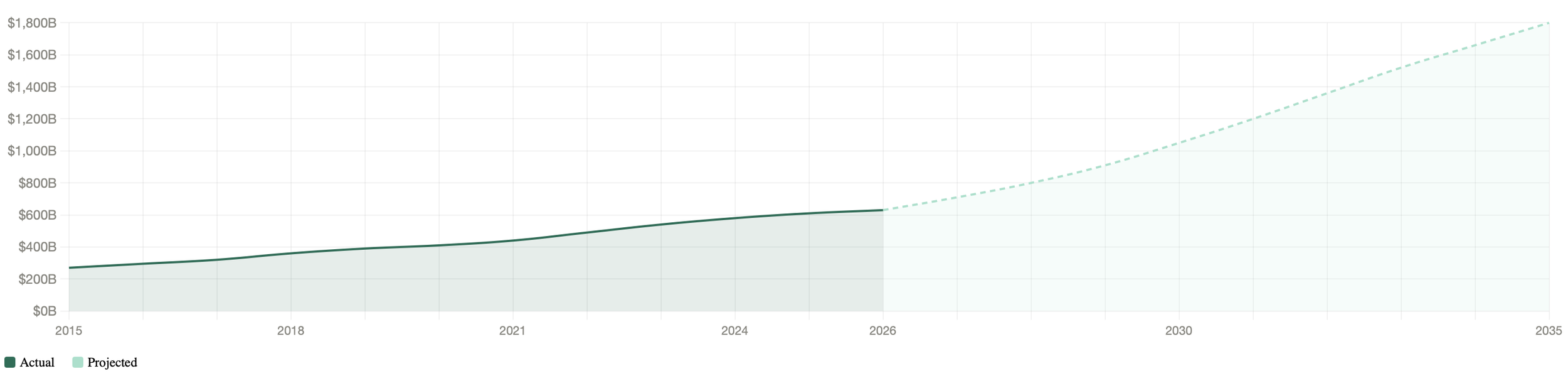

The numbers frame the scale of what is coming. The global space economy stands at approximately $630 billion today. By 2035, it is projected to reach $1.8 trillion — nearly three times its current size. That growth will not be delivered by SpaceX alone. It will require an entire ecosystem of specialised companies across launch, satellite operations, ground infrastructure, data analytics, propulsion, materials and orbital logistics. Many of those companies are still private. Many are still small. And almost all of them will need significant capital to reach their potential.

Area chart showing global space economy growth from 2015 to 2035, projected to reach $1.8 trillion

The publicly listed segment of this ecosystem is already taking shape, offering investors early visibility into the sector’s breadth:

• Firefly Aerospace (FLY) — A launch and spacecraft company with a $1.4 billion contract backlog, directly integrated into the Golden Dome defence architecture. One of the more credible pure-play launch alternatives to SpaceX in the public markets

• Rocket Lab (RKLB) — Small satellite launch and spacecraft manufacturer, trading at approximately 123x sales, reflecting the market’s appetite for space exposure even at steep multiples

• AST SpaceMobile (ASTS) — Building a space-based cellular broadband network, targeting direct-to-device connectivity for standard mobile phones globally

• Intuitive Machines (LUNR) — NASA contractor focused on lunar logistics and surface operations, positioned at the heart of the Artemis programme

• Redwire Corporation (RDW) — Space infrastructure manufacturer producing solar arrays, booms and deployable structures for both commercial and government missions

• BlackSky (BSKY) — Real-time geospatial intelligence and satellite imaging, serving defence and intelligence customers

• Graham Corporation (GHM) — Specialist manufacturer of energy and defence equipment with growing space sector exposure

• York Space Systems (YSS) — Small satellite manufacturer serving government and commercial customers, backed by AE Industrial Partners

The private company landscape is where the PE opportunity becomes most pronounced. Away from public markets, a generation of highly specialised businesses is quietly building the components, systems and services that the space economy runs on:

• Voyager Space — Deep space exploration and low Earth orbit infrastructure, backed by RedBird Capital and targeting NASA’s next generation of crewed missions

• Astranis — Small geostationary satellite operator delivering dedicated broadband to underserved markets, backed by Andreessen Horowitz

• ICEYE — Finnish radar satellite constellation operator valued above $2.5 billion, providing persistent monitoring for insurance, disaster response and defence

• Pixxel — Hyperspectral imaging satellites delivering agricultural, environmental and industrial intelligence

• LeoLabs — Space debris tracking and collision avoidance, an increasingly critical service as orbital congestion grows

• Relativity Space — 3D-printed rocket manufacturer targeting a fully reusable launch vehicle, one of the most watched private space companies globally

The government tailwind underpinning all of this is unlike almost anything else in the investment landscape. Space Force, Golden Dome, NASA’s Artemis lunar programme, allied nation defence contracts and the emerging market for sovereign satellite infrastructure collectively provide a revenue floor that fundamentally de-risks the private capital story. These are not discretionary budgets — they are strategic national priorities with multi-decade spending commitments behind them.

And then there is the consumer dimension, still nascent but accelerating. Blue Origin has operational tourist flights. The successor vehicles to Virgin Galactic are in development. Within a decade, sub-orbital and orbital tourism will transition from novelty to niche industry, adding a demand layer that government contracts alone cannot capture. The sketch of a future where space travel becomes genuinely mass-market — not in five years, but in twenty — is no longer science fiction. It is a capital planning assumption.

For PE investors, the parallel that keeps surfacing is the semiconductor industry in the early 1990s. A transformational technology, enormous capital requirements, highly specialised supply chains, and a window of perhaps ten years in which patient, informed capital could establish positions in companies that would define the next half century. The investors who understood that moment built generational returns. The investors who waited for certainty bought in at the top.

Space is that moment. It is earlier, messier and less certain than semiconductors were in 1995. But the trajectory is visible, the government backing is structural, and the exit architecture — as of this morning — is finally in place.

One Small Step for Markets

There is a phrase that gets overused in financial commentary — “historic moment.” It is applied to quarterly earnings beats, to rate decisions, to merger announcements that are forgotten within a year. Today it is not hyperbole. It is the only accurate description.

What has happened this week in global capital markets is without precedent. The largest IPO in history, priced at nearly twice the previous record. A quarter of a trillion dollars mobilised by institutional investors in pursuit of a single offering. A company valued at $1.77 trillion — built on rockets, satellites, artificial intelligence and the audacious belief that human civilisation should become multiplanetary — now trading on the Nasdaq alongside the banks, the technology giants and the consumer brands that have defined the investment landscape for the past three decades.

SpaceX’s arrival in public markets is not simply a liquidity event for early investors and employees. It is a structural moment for the entire investment ecosystem. It establishes space as a legitimate, benchmarkable, exit-capable asset class for the first time. It sets a valuation framework that will ripple through every growth equity conversation, every LP committee meeting and every sector allocation decision that touches the space industry for the next decade. And it signals, unmistakably, that the era of space as a speculative fringe — interesting but uninvestable at institutional scale — is over.

For the private equity community specifically, the implications are profound and immediate. The unclogging effect is real. Capital that has been circling the sector cautiously, waiting for proof of exit, now has its proof. The companies building the infrastructure of the space economy — the launch providers, the satellite operators, the propulsion specialists, the orbital data platforms — are no longer a bet on an uncertain future. They are an early position in an industry whose trajectory is now anchored by the most watched public listing in a generation.

The broader financial world should take note of something else. SpaceX’s IPO arrives alongside confirmed SEC filings from both OpenAI and Anthropic. Three companies — each defining a different dimension of humanity’s technological future — preparing to enter public markets within a single twelve month window. The capital markets are being asked to absorb, price and sustain the valuation of the AI era, the space era and the connectivity era simultaneously. Whether markets prove equal to that task will be one of the defining financial narratives of the late 2020s.

But zoom out further still. What trades today on the Nasdaq is not merely a stock. It is a statement of ambition — corporate, national and civilisational. The same company that made rockets reusable, that built the internet from orbit, that is laying the groundwork for data centres in space and boots on Mars, has decided that the public markets are ready for it.

NEEM believes we are witnessing the birth of a new asset class, and that the firms which recognise this moment for what it is will look back on today as the starting gun.