The Shadow Lender

How Private Credit Became the Fuel Behind the AI Arms Race

What Is Private Credit?

When most people think of borrowing money, they think of banks. A company needs capital, it walks into a bank, the bank lends it money and charges interest. For most of the twentieth century, that was how corporate finance worked. Private credit is the alternative - and it is rapidly becoming the dominant one.

In private credit, the lender is not a bank but a fund. Institutional investors - pension funds, sovereign wealth vehicles, family offices - pool their capital into a private credit vehicle, which then lends directly to companies. The borrower gets its capital. The fund collects interest. The investors receive a yield that, in recent years, has consistently sat between eight and twelve percent — well above what bonds or public markets could offer.

The mechanics differ from bank lending in three important ways. First, the loans are illiquid - they cannot be traded on a public market, and investors commit their capital for years at a time. Second, the interest rate is almost always floating, meaning it moves in line with central bank rates rather than being fixed at the outset. Third, loans typically come with covenants - conditions the borrower must maintain, such as keeping debt below a certain multiple of earnings. These covenants give the lender early warning signs and intervention rights if a borrower begins to struggle.

Private credit sits between bank lending and private equity in the financial ecosystem. It is less risky than equity — lenders are repaid before shareholders in any restructuring — but higher yielding than public bonds, which compensate for their liquidity with lower returns. For the right investor, it occupies a compelling middle ground: predictable income, real security, and yields that make other fixed income look anaemic.

Why Has It Been Rising Ever Since 2008?

Private credit did not become a $3.5 trillion asset class by accident. It was built, largely, on the wreckage of the global financial crisis - and then supercharged by a decade of policy decisions that made it structurally inevitable.

When Lehman Brothers collapsed in 2008, regulators across the developed world drew the same conclusion: banks had taken on too much risk, with too little capital to absorb losses. The response was Basel III - a sweeping overhaul of banking regulation that forced banks to hold significantly more capital against risky loans. The practical consequence was predictable. Mid-market lending, leveraged buyout financing, real estate debt, infrastructure loans - the categories that private credit would go on to dominate - became uneconomical for regulated banks. The risk-adjusted returns simply did not justify the capital requirements. Banks retreated. A gap opened. Private credit funds stepped in.

That was the supply side of the story. The demand side was equally powerful. In the aftermath of the crisis, central banks held interest rates near zero for over a decade. For institutional investors - pension funds managing retirement obligations, endowments seeking stable returns, family offices preserving and growing multigenerational wealth - this created an acute problem. The assets they had historically relied upon for income: government bonds, investment grade corporate debt, money market instruments, were yielding next to nothing. A ten-year US Treasury bond yielded under two percent for most of the 2010s. Private credit, offering eight to twelve percent on secured loans to real businesses, was not just attractive, it was the only credible source of yield in the portfolio.

Then came 2022, and what should have been private credit's crisis moment turned into its greatest acceleration. The Federal Reserve raised rates from near zero to over five percent in eighteen months - the sharpest tightening cycle in four decades. For fixed income investors, rising rates meant falling bond prices and portfolio losses. For private equity, expensive debt froze dealmaking entirely. But private credit funds, with their floating rate loan books, saw their income rise automatically as rates climbed. The asset class that was supposed to struggle in a rising rate environment became, paradoxically, one of the best places to be. Capital flooded in.

The New Frontier: Private Credit Meets the AI Arms Race

If the first phase of private credit's rise was about filling the gap left by retreating banks, the second phase is about something far more ambitious - financing the most capital-intensive technology buildout in human history.

The artificial intelligence arms race requires infrastructure at a scale that strains the imagination. Data centres the size of small towns. Power infrastructure measured in gigawatts. Cooling systems, fibre networks, GPU clusters costing tens of thousands of dollars per unit. JP Morgan estimates that $5.3 trillion will be needed to support AI infrastructure development through 2030. The hyperscalers - Meta, Microsoft, Google, Amazon - are spending at a rate that dwarfs anything seen in previous technology cycles. And increasingly, they are turning to private credit to fund it.

The logic is straightforward. Public bond markets can absorb large issuances, but they are slow, regulated, and put debt visibly on the balance sheet for every analyst and shareholder to scrutinise. Private credit offers something different: speed, flexibility, bespoke structuring, and crucially, the ability to finance assets through special purpose vehicles that keep the borrowing off the parent company's headline accounts. For a hyperscaler managing analyst expectations while simultaneously spending hundreds of billions on infrastructure, that discretion has real value.

The deal that crystallised this dynamic was struck in 2025, when Meta created a special purpose vehicle to finance its Hyperion data centre campus in Louisiana - the largest private credit transaction ever recorded. Blue Owl Capital led a consortium providing $27 billion in debt alongside $3 billion in equity. A single transaction. One data centre campus. Twenty-seven billion dollars in private credit. Nearly $200 billion in total debt was raised for data centre development across the market in 2025 alone — a 57 percent increase on the prior year.

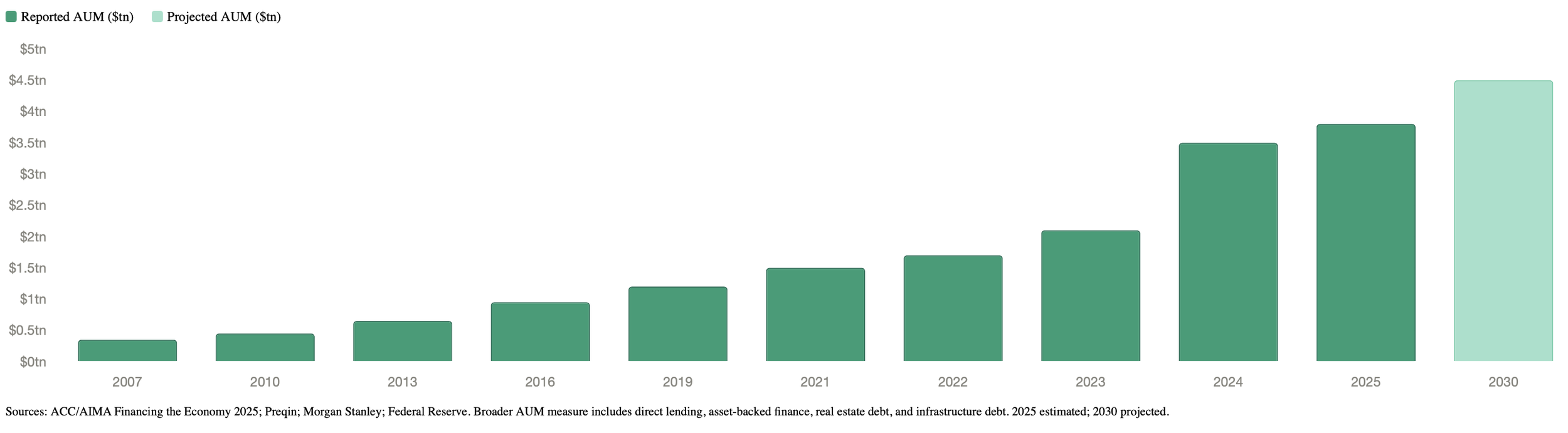

Private Credit AUM Growth 2007–2030

The numbers tell a story of an asset class that has outgrown its origins. From $350 billion in assets under management in 2007, private credit has expanded to $3.5 trillion by end of 2024 marking a ten-fold increase in under two decades, and is projected to reach $4.5 trillion by 2030. The major alternative asset managers have reorganised themselves around it entirely. Apollo's private credit AUM now represents 82 percent of its total assets. Ares Management's private credit segment comprises 72 percent of total assets. Private credit is no longer an alternative to the mainstream - it is the mainstream.

The Risks Nobody Is Pricing

Every asset class that grows ten-fold in two decades accumulates risks alongside returns. Private credit is no exception and the risks building inside it are, by design, difficult to see.

The first and most fundamental problem is opacity.

Unlike public bonds, which are priced daily by the market, private credit valuations are self-reported by the funds that hold them. There is no independent mark. When a borrower begins to struggle, a private credit manager faces a choice that a public bond manager does not: recognise the stress immediately, or restructure quietly and extend the loan's maturity. Increasingly, the industry has chosen the latter. Payment-in-kind loans, where a struggling borrower is permitted to roll unpaid interest into the principal rather than paying cash, have proliferated across the market. The loan appears performing on paper. The borrower is quietly drowning. Regulators and industry experts have warned that default rates and financial distress in private credit are being systematically underreported as a result.

The second risk is covenant erosion.

The protections that were supposed to distinguish private credit from the more permissive public loan markets have been progressively weakened as competition for deals intensified during the boom years. Covenant-lite and so-called cov-loose structures now dominate new issuances. The consequence is that lenders lose the ability to intervene proactively when a borrower deteriorates. By the time a formal default is triggered, the damage is already done.

The third risk is the one least discussed and potentially the most consequential.

Private credit has, in large part, become a financing mechanism for the AI infrastructure boom. And the AI infrastructure boom is currently spending at a rate that its revenues cannot justify. The industry generated approximately $60 billion in revenue in 2025 against roughly $400 billion in capital expenditure which is a seven-to-one ratio of spending to earnings. The loans funding Meta's data centres, Oracle's Stargate commitments, and hundreds of smaller AI infrastructure projects are ultimately a bet that AI monetisation will grow fast enough to service that debt. If it does not - if the AI revenue ramp disappoints, or if the technology cycle turns before the infrastructure pays for itself - the stress will migrate directly into private credit portfolios. The problem is that most LP investors in private credit funds have no clear visibility into how much AI concentration risk they actually hold. The opacity that masks individual loan stress also masks portfolio-level thematic exposure.

The interconnectedness compounds all three risks. As of late 2024, US banks had extended $95 billion in committed credit lines to private credit funds meaning that a stress event in private credit would not stay contained within the asset class. It would ripple back into the regulated banking system through those credit lines, potentially triggering the kind of second-order contagion that regulators have been warning about since the asset class began its ascent.

What Comes Next - And Should You Be Worried?

The instinctive response to a $3.5 trillion market built on opaque valuations, eroded covenants, and concentrated AI exposure is alarm. The more considered response is nuance because the picture is genuinely more complex than either the bulls or the bears acknowledge.

The systemic catastrophe scenario appears, for now, contained. The Federal Reserve's June 2025 stress tests were explicit on the point: private credit and hedge funds do not pose a systemic risk to the US banking system. Even under severe recession scenarios, banks maintained capital ratios above minimum requirements, with limited contagion from non-bank financial intermediaries. The 2008 playbook - frozen interbank lending, solvency crises cascading through interconnected balance sheets - does not map cleanly onto the private credit structure, where 80 percent of assets sit in closed-ended, long-duration vehicles with institutional capital that is not redemption-sensitive. There will be no bank run on a ten-year locked-up fund.

But the absence of systemic crisis is not the same as the absence of pain. What is coming, and what the more honest voices in the industry are already acknowledging, is a bifurcation. Howard Marks of Oaktree Capital put it plainly in November 2025: the worst loans are made in the best of times. The funds that deployed capital aggressively during the 2021–2023 boom, relaxed their covenant standards to win deals, and built concentrated exposure to AI infrastructure borrowers without stress-testing the revenue assumptions are going to face a reckoning. Not a collapse, but a long, grinding period of restructurings, maturity extensions, and returns that fall well short of what was promised to LPs.

The funds that maintained discipline - rigorous covenant structures, diversified borrower bases, genuine credit analysis rather than yield-chasing - will continue to perform. Private credit as a structural financing mechanism is not going away. The gap left by retreating banks is real and permanent. The capital needs of an AI-driven economy are not shrinking. The asset class will reach $4.5 trillion by 2030 almost regardless of what happens in the next two years. But the quality of that growth - who is lending to whom, on what terms, against what collateral - will determine whether the next chapter of private credit is defined by the managers who built the asset class carefully, or by those who rode its momentum carelessly.

For limited partners, the implication is the same one that runs through every corner of alternative assets in this cycle: the era in which any exposure to a growing asset class generated acceptable returns is over. Private credit is not a category decision anymore. It is a manager decision - and increasingly, it is a question of whether your manager has the transparency, the credit discipline, and the sector judgment to navigate what comes next.

NEEM believes that private credit, selectively deployed through managers with genuine underwriting rigour, remains one of the most compelling structural opportunities in alternatives today. The shadow lender has stepped permanently into the mainstream. The question is which shadow lenders you trust with your capital.