The Vintage Window

Why 2025–2026 May Define the Next Decade of PE Returns

The best vintages in private equity are rarely recognised as such at the time.

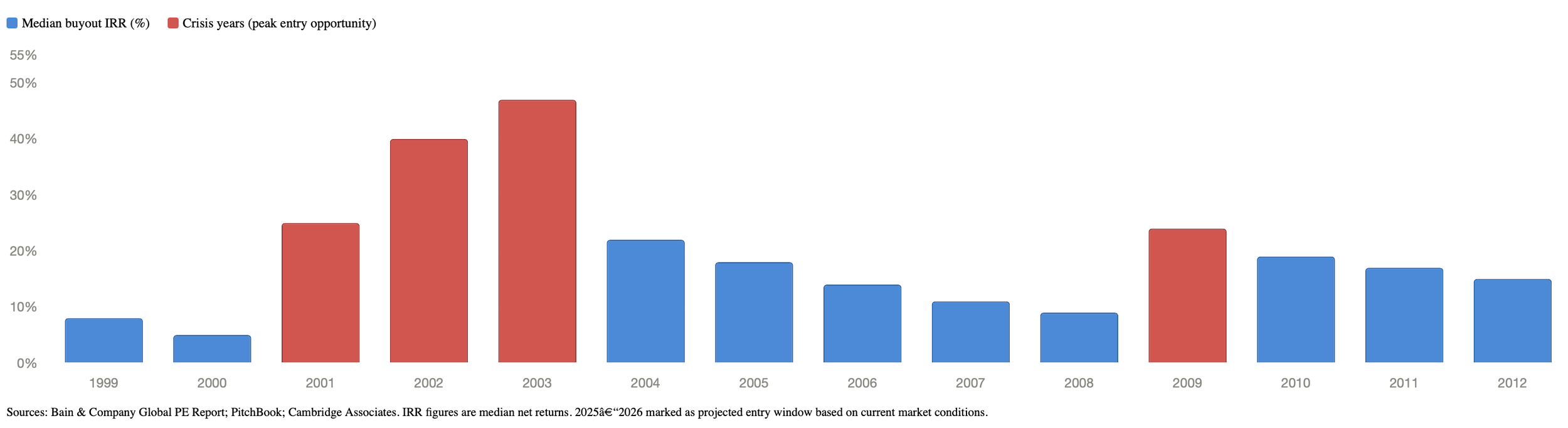

In 2001, as the dot-com wreckage was still smouldering, buyout funds that deployed capital into the rubble went on to generate median IRRs of 25 percent. The following year, 40 percent. The year after, 47 percent. In 2009, as bank balance sheets were being restructured and the word "recession" dominated every headline, funds that committed capital posted 24 percent returns.

The pattern is not coincidental. Private equity rewards those who invest when others will not - and penalises, often severely, those who wait until confidence returns and prices reflect it.

How We Got Here: The COVID Reckoning

The conditions that produce golden vintages do not announce themselves. They accumulate quietly, through a sequence of macro events that most investors experience as headwinds rather than opportunity. What has unfolded in private equity since 2022 is precisely such a sequence.

In March 2020, central banks across the developed world did something without modern precedent: they printed money at scale, simultaneously, to prevent economic collapse. Interest rates were held near zero. Governments injected trillions in fiscal stimulus. The intention was survival. The consequence, two years later, was the sharpest inflation spike in four decades - and the most aggressive rate-hiking cycle since the 1980s to contain it. The US Federal Reserve raised rates from near zero to over 5% in eighteen months.

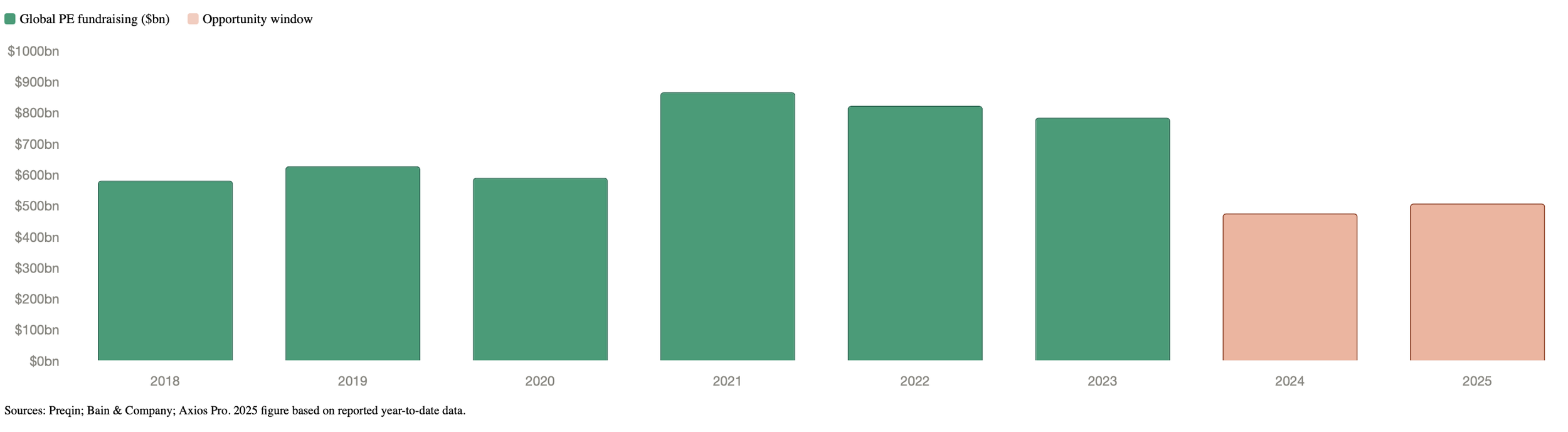

For private equity, this was a seismic shift. The asset class had operated for over a decade in an environment of structurally cheap debt. Buyouts that once relied on 3% financing now faced 7% or 8%. Companies acquired at peak valuations in 2021, at the height of the easy-money frenzy, suddenly could not generate enough cash flow to service their leverage. Deal activity froze. Sellers clung to yesterday's valuations. Buyers repriced risk overnight. The result was a standoff that paralysed the market for the better part of two years, and a fundraising collapse that sent capital raised from an $867 billion peak in 2021 to $476 billion by 2024 - the lowest level of fund closures since 2008.

Global PE Fundraising 2018–2025

The Window Is Open - But Not for Long

That freeze is now thawing - but unevenly, and that unevenness is precisely where the opportunity lies.

Exits are recovering. Global PE exit value rebounded strongly in 2025, and the IPO market, dormant since 2022, is showing genuine signs of life. The Medline IPO in late 2025, the largest PE-backed public offering in four years, was not an anomaly but a signal: the exit ecosystem is functional again. Buyers and sellers are closing the valuation gap that kept dealmaking suspended. Financing conditions, while not returning to the zero-rate era, are stabilising at levels that allow disciplined transactions to work.

Yet fundraising has not recovered in step. Capital commitment to new PE funds remains well below its 2021 peak, and the average time to close a fund has extended from eleven months in 2022 to over two years today. Limited partners, still waiting on distributions from their 2021 vintage commitments, are cautious about writing new cheques.

This lag - between improving deal conditions and the return of institutional capital - is the window. It is the same dynamic that made 2001 and 2009 exceptional: the market was healing before most investors were willing to believe it.

The opportunity is most acute in the lower mid-market. At the upper end, megafunds with hundreds of billions in dry powder continue to compete aggressively, keeping entry multiples above 11x EBITDA.

But in the $25 to $100 million enterprise value range - where most emerging companies operate, and where proprietary sourcing still determines deal access - multiples remain in the six to eight times range. Less competition. Better prices. The same eventual exit market. The broader exit environment, meanwhile, continues to improve. The anticipated public listings of OpenAI and Anthropic, at valuations approaching two trillion dollars, will serve as a meaningful test of public market appetite. If they land well, they will likely accelerate the reopening of the IPO window for PE-backed businesses more broadly, reinforcing the case that 2026 marks the beginning of a durable exit cycle rather than a temporary thaw.

The End of Easy Money And Why It Changes Everything

But timing the market is only half the equation. The other half, the one that separates this cycle from every previous one, is what you do once you are in it.

For the decade that ended in 2022, private equity returns were flattered by three structural tailwinds that had nothing to do with skill.

Cheap debt amplified returns mechanically. With borrowing costs near 3%, firms could finance the majority of an acquisition with debt, magnifying equity returns without any operational improvement. The leverage did the work.

Multiple expansion gave every manager a free ride. As interest rates fell year after year, the same earnings stream was worth more each year in discounted value terms. A business bought at 8x earnings could be sold at 11x five years later - not because it improved, but because the market re-rated it upward automatically.

Benign macro conditions ensured portfolio companies grew revenues almost by default. Cheap mortgages, accessible corporate credit, and steady consumer demand meant that even mediocre businesses posted respectable top-line growth throughout the holding period.

The combined effect was a decade in which the market was generating returns that looked like alpha but were, in large part, beta dressed up in carry.

That era is over. Debt costs 7%-8%. Multiples are not expanding - if anything, the pressure runs the other way. McKinsey's 2026 private markets report was blunt on the point: alpha must be made, not assumed. Apollo, in its own year-ahead assessment, put it more directly still - the era of buying good companies at any price and waiting for the market to bail you out has ended. What remains is the original promise of private equity: buy intelligently, improve relentlessly, exit with discipline.

This shift has a direct consequence for limited partners. When tailwinds do the heavy lifting, manager selection matters less - most funds in a rising tide deliver acceptable returns. When those tailwinds are gone, the dispersion between top-quartile and bottom-quartile managers widens dramatically. The difference between backing the right GP and the wrong one is no longer a matter of a few percentage points. It is the difference between realised returns and stranded capital.

Vintage Year IRR by Year 1999–2012

The Question Is Not Whether. It Is Who.

The question, then, is not whether to deploy capital into private equity. The historical evidence on that is unambiguous - the funds raised in the aftermath of dislocation consistently outperform those raised at the peak of confidence. The question is who you deploy it with.

In an environment where returns must be earned rather than received, the edge belongs to managers with genuine sector expertise, proprietary sourcing relationships, and the operational depth to improve businesses rather than simply hold them. Generalist strategies that rely on financial engineering are facing their most challenging environment in a generation. Specialist managers - those who understand the structural forces reshaping specific industries, who can identify emerging companies before they enter competitive auction processes, and who bring more than capital to the table - are positioned to generate the kind of returns that defined the great vintages of the past.

The window is open. It will not remain so indefinitely. As distributions recover, as LP confidence returns, and as institutional capital flows back into the asset class, entry conditions will tighten and competition will intensify. The investors who recognise this moment for what it is will look back on 2025 and 2026 the way the best managers look back on 2001 and 2009. Not as years they survived. As years they built their best returns.

NEEM believes the window is open, the conditions are right, and that in an era where alpha must be earned, specialist expertise is no longer an advantage - it is the only thing that matters.